(1) The estimated annualised yield is calculated based on the investment price set by the investor (buy and sell prices), as well as the specific number of days the bond is held, to determine the annualised rate of return for the bond during the holding period. This rate of return only considers capital gains (or losses) and interest income during the holding period.

(2) The Yield to Maturity (YTM) of a bond refers to the expected annualised rate of return if the bond is held to maturity, and all interest payments are reinvested at the same rate throughout the period. YTM is a more comprehensive method of measuring bond yields as it takes into account all future interest payments and the repayment of principal at maturity, assuming that all interest can be reinvested at the same rate as the YTM.

(3) Reasons for the discrepancy between the estimated annualised yield and YTM may include:

Reinvestment assumption: YTM assumes that all interest is reinvested at the same yield, while the estimated annualised yield does not make this assumption.

Holding period: The estimated annualised yield is calculated based on the actual number of holding days, while YTM assumes the bond is held to maturity.

Treatment of principal at maturity: YTM takes into account the repayment of principal at maturity, while the estimated annualised yield typically only focuses on the difference between the buy and sell prices.

Market interest rate fluctuations: Changes in market interest rates can affect the sell price and thus impact the estimated annualised yield, but YTM is a fixed value calculated at the time of purchase based on market conditions at that time.

US Treasuries Yields

- US 2Y T-Notes Yield3.486+0.008 +0.24%

- US 5Y T-Notes Yield3.751+0.021 +0.56%

- US 10Y T-Notes Yield4.195+0.016 +0.38%

- US 20Y T-Notes Yield4.822+0.018 +0.36%

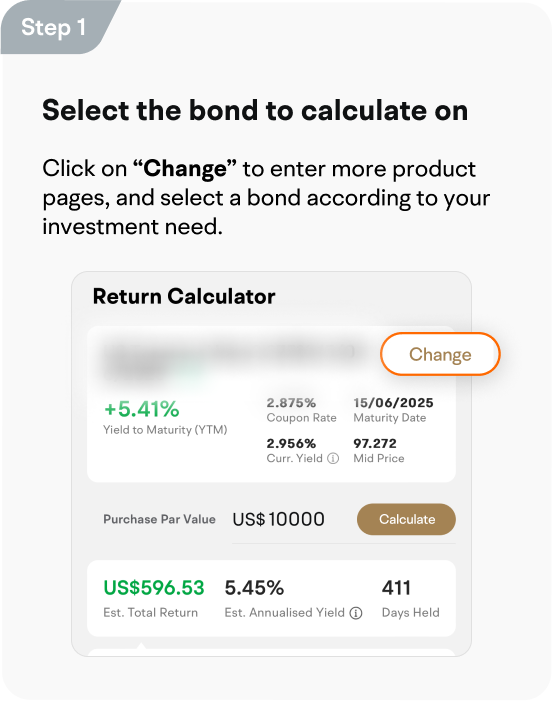

Return Calculator

*Date of update: 05/01/2026. Displayed are all US Treasuries and SGS bonds with tenor of over 1 months, available on the moomoo platform, sorted by daily yield to maturity from highest to lowest.

How to use the

Bond Return Calculator?

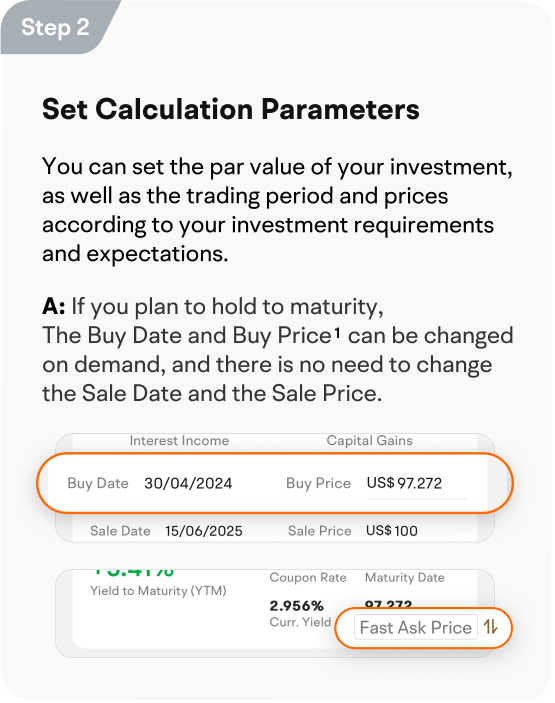

- 1. Buy Price: defaulted to [Mid Price], if the bond support Fast Trade feature, it can switch to [Fast Ask Price]

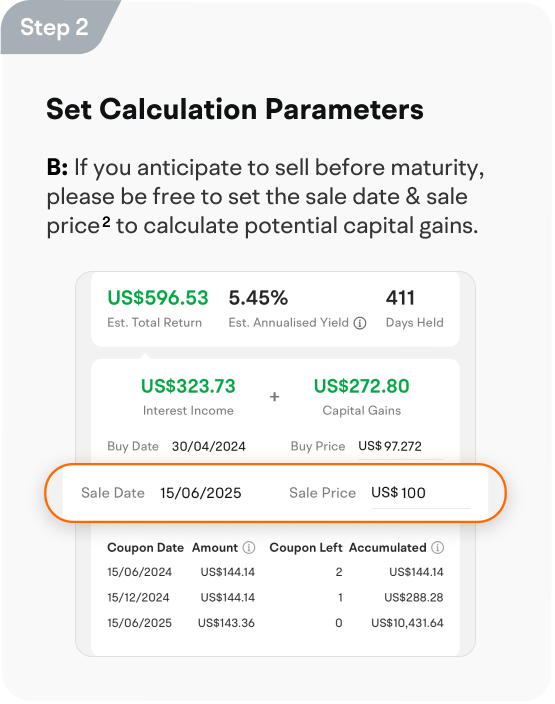

- 2. Sale Date: default by the maturity date of the Bonds;

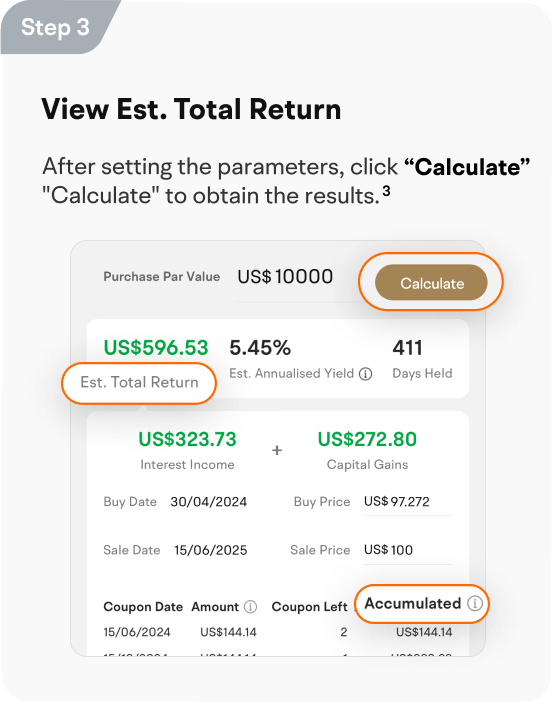

Sale Price: default by the par value recovered at maturity. - 3. Estimated Total Returns = Interest Income + Capital Gains. The estimated total returns reflect the investment return over the holding period. Earnings Accumulated = Purchase Face Value or Sale Proceeds + Total Interest Payments. The cash inflow is only taken into consideration during the bond holding period.

FAQs

1. Why is the annualised yield calculated by the calculator inconsistent with the data shown on the product detail page?

2. How to buy bonds?

(1) Select the bond you want to trade in the bond list or in the search results, and then tap the Buy button on the bond details page.

(2) Enter the nominal value and the buying price you desire. You can refer to the "Indicative Ask Price". (This price is for reference only and may differ from the actual transaction price.)

(3) Tap the Buy button, enter your transaction password, and submit the order. Please wait patiently for the order to be matched. The transaction price will not exceed the order price.

3. Why is my order not executed immediately after being submitted?

Since bonds are traded over the counter and brokers are needed to match orders, transaction time and prices are influenced by various factors such as daily market liquidity and counterparty conditions. You can try to increase the buying price or decrease the selling price, or wait patiently for the right counterparty or market price.

【New Features】Explore Fast Trade for Bonds to Enhance Your Investing Experience!

4. Must bonds be held to maturity?

No, it can be held until maturity or sold in advance at any trading time.

5. When can interest be earned? And, can I still receive interest the bond is not held till the payment date?

The accrued interest on bonds has 2 parts: Firstly, the interest paid to the seller at the time of purchase. The other is the interest accumulated during the holding period with interest being earned for each holding day.

Both parts of the interest will be paid to investors on the interest payment date. Investors can estimate whether they will receive interest on the next interest payment date based on whether the accrued interest they hold is approximately equal to for example, semi-annual interest.

Additionally if the bondholder sells the bond before the interest payment date, the buyer should pay the accrued interest to the seller.6. Tax Considerations for Investing in US Treasuries

In most cases, purchasing US Treasuries does not require paying taxes for non-U.S. residents.

However, specific tax regulations may vary depending on individual circumstances and the type of US Treasuries invested in. Therefore, it is advisable to consult with tax professionals to obtain accurate tax information.

More Details

Related Content

US Treasury Investment Strategies

Understand the 3 most common scenarios in one article >>

Introduction: US Treasuries, growing your cash

Low investment risk | Regular interest payment | Predictable returns >>

Introducction: Singapore Government Securities

Backed by AAA credit rating | Regular earnings| Tax exempt for individuals | Starting from S$1,000 >>

Moomoo Feature: Fast Trade

Explore Fast Trade for Bonds to Enhance Your Investing Experience!

Please note

1. Although defaults by the U.S. government are extremely rare, there is still a risk of default. Political, fiscal conditions, or other factors may lead to the government being unable to repay its debt on time or in full. While this risk is low, it cannot be completely eliminated.

2. Additionally if you are a non-U.S. investor holding onto US Treasuries, it may expose you to foreign exchange risk. Exchange rate fluctuations may affect the return on your investment, causing variability when calculated in your local currency.

3. Before making any investment, please carefully assess your risk tolerance and consult with investment advisors or professionals for more accurate and personalised investment advice.

4. The Return calculation data displayed on this page is for reference only. It does not guarantee the actual performance of returns that investors may receive in the future, nor does it constitute any investment advice.

Disclaimer

1. In Singapore, investment products and services available through the moomoo app are offered through Moomoo Financial Singapore Pte. Ltd. regulated by the Monetary Authority of Singapore (MAS).

2. Any estimations calculated are for informative purposes and does not take into account any fees and charges, should not rely on it solely for your decision making process.

3. No content herein shall be considered an offer, solicitation or recommendation for the purchase or sale of securities, futures, or other investment products.

4. Moomoo SG will act as your agent when providing services of U.S. Treasuries to you.

5. All types of investments are risky and investors may suffer losses. All information and data on the website are for reference only. Past performance does not guarantee future results.

6. This advertisement has not been reviewed by the Monetary Authority of Singapore.

More details

© 2025 moomoo